Understanding Current Mortgage Rates: A Comprehensive Guide For Homebuyers

In today's ever-evolving financial landscape, current mortgage rates play a crucial role in determining the affordability of homeownership. Whether you're a first-time buyer or looking to refinance, understanding mortgage rates can significantly impact your financial future. This article will provide an in-depth exploration of mortgage rates, empowering you to make informed decisions about one of the most significant investments of your life.

Mortgage rates fluctuate based on various economic factors, making it essential for borrowers to stay updated. A slight change in rates can affect monthly payments and overall loan costs. By staying informed, you can secure the best possible mortgage terms and take advantage of favorable market conditions.

This guide is designed to demystify the complexities of mortgage rates. From explaining how rates are determined to offering practical tips for securing the best deals, we aim to equip you with the knowledge needed to navigate the mortgage market confidently. Let's dive into the details.

- Gpix Dividend Yield

- Detective Lisa Charles Nassau County

- 100 Dollar Bill On Windshield

- Alysha Nelson

- Mcdonalds The Grinch

Table of Contents

- Introduction to Mortgage Rates

- Factors Affecting Current Mortgage Rates

- Types of Mortgage Loans

- How Are Mortgage Rates Determined?

- Current Mortgage Rates Trends

- How to Compare Mortgage Rates

- Tips for Getting the Best Mortgage Rates

- Common Mistakes to Avoid

- The Future of Mortgage Rates

- Conclusion and Next Steps

Introduction to Mortgage Rates

Mortgage rates represent the cost of borrowing money to purchase a home. These rates are expressed as an annual percentage of the loan amount and are a critical factor in determining the total cost of homeownership. Understanding how mortgage rates work is essential for anyone planning to buy a property or refinance an existing mortgage.

What Are Mortgage Rates?

Mortgage rates are the interest rates charged by lenders for financing a home purchase. They vary based on factors such as the type of loan, borrower's creditworthiness, and prevailing economic conditions. Borrowers with higher credit scores typically qualify for lower rates, reducing their overall borrowing costs.

Why Are Mortgage Rates Important?

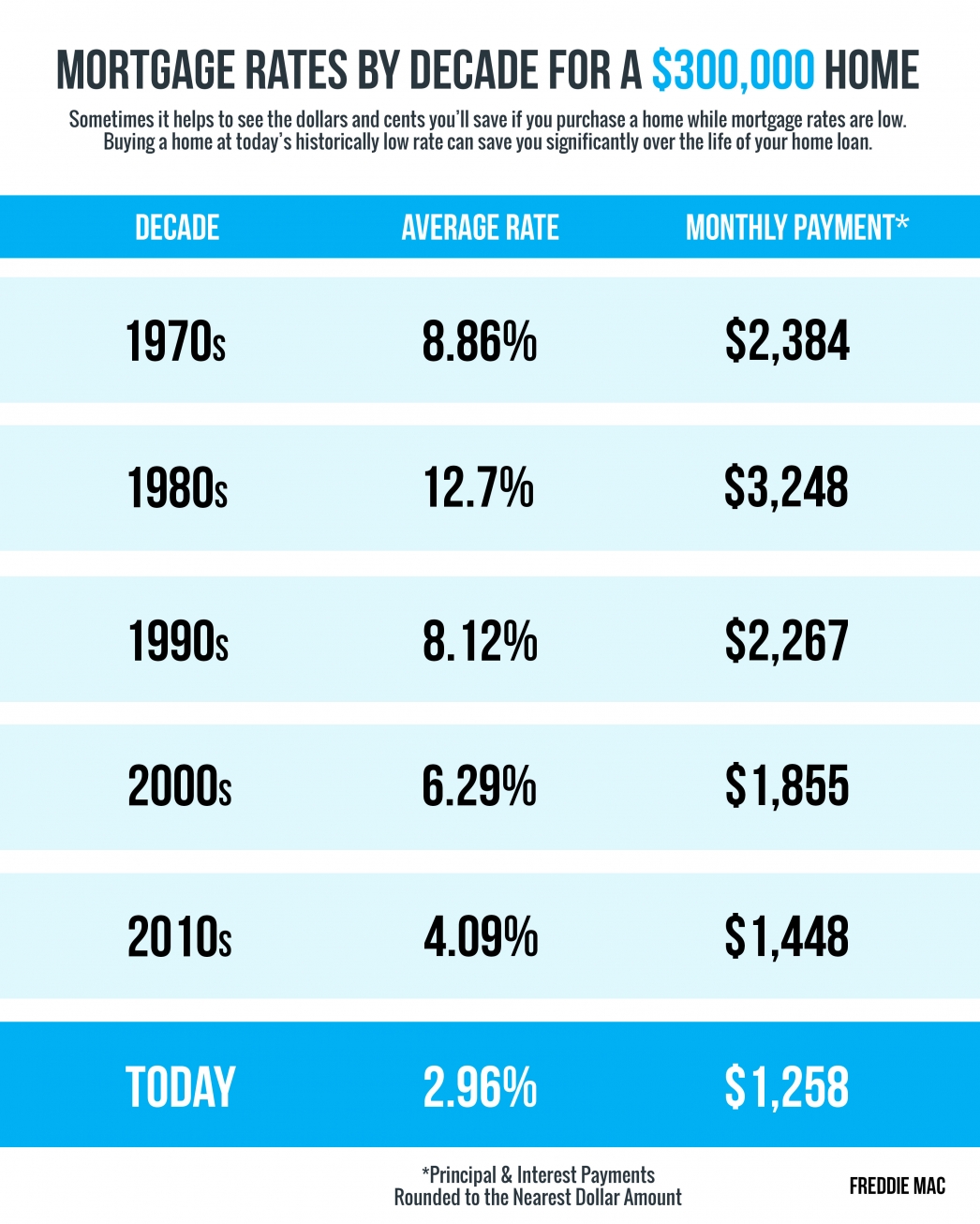

Mortgage rates directly impact monthly payments and the total amount paid over the life of the loan. Even a small difference in rates can result in significant savings or additional costs. For example, a 0.5% difference in a 30-year fixed-rate mortgage can save or cost thousands of dollars over the loan term.

- Paris La Defense Christmas Market

- Gator Cove Seafood Restaurant

- Carol Channing Daughter

- Final Grades Ut

- Rob Moore Executive

Factors Affecting Current Mortgage Rates

Several key factors influence current mortgage rates. Understanding these factors can help you anticipate rate changes and make timely decisions about purchasing or refinancing a home.

Economic Conditions

Economic factors such as inflation, unemployment rates, and gross domestic product (GDP) growth impact mortgage rates. During periods of economic uncertainty, rates may rise due to increased borrowing costs for lenders.

Federal Reserve Policies

The Federal Reserve's monetary policies, including changes to the federal funds rate, indirectly affect mortgage rates. When the Fed lowers interest rates, mortgage rates tend to follow suit, making borrowing more affordable for consumers.

Bond Market Performance

Mortgage rates are closely tied to the performance of the bond market. When demand for mortgage-backed securities (MBS) is high, rates tend to decrease. Conversely, a decline in MBS demand can lead to higher mortgage rates.

Types of Mortgage Loans

There are various types of mortgage loans, each with its own rate structure and terms. Choosing the right loan type depends on your financial situation and long-term goals.

Fixed-Rate Mortgages

Fixed-rate mortgages offer a consistent interest rate throughout the loan term, providing stability and predictability in monthly payments. These loans are ideal for borrowers who plan to stay in their homes for an extended period.

Adjustable-Rate Mortgages (ARMs)

Adjustable-rate mortgages feature fluctuating interest rates tied to market indices. While initial rates may be lower than fixed-rate loans, they can increase over time, making them suitable for short-term homeowners or those expecting interest rates to remain stable.

How Are Mortgage Rates Determined?

Mortgage rates are influenced by a combination of borrower-specific and broader economic factors. Lenders assess risk levels and market conditions to set rates that balance profitability and affordability.

Borrower Credit Score

A borrower's credit score is a critical determinant of mortgage rates. Higher scores indicate lower risk, allowing lenders to offer more favorable terms. Maintaining good credit is essential for securing the best rates.

Loan-to-Value Ratio (LTV)

The loan-to-value ratio compares the loan amount to the property's value. Lower LTV ratios reduce lender risk, often resulting in better mortgage rates. Making a larger down payment can improve your LTV and qualify you for more competitive rates.

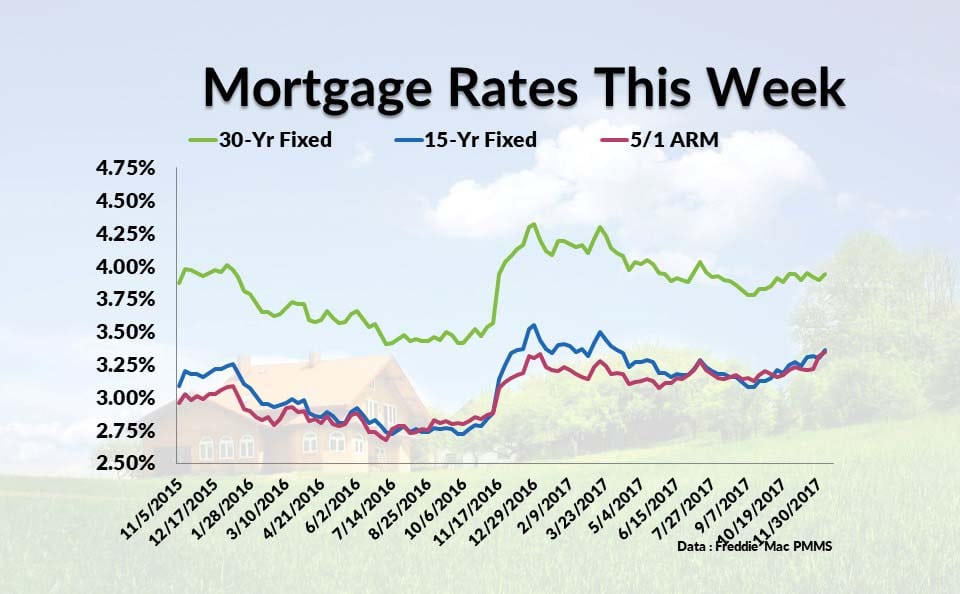

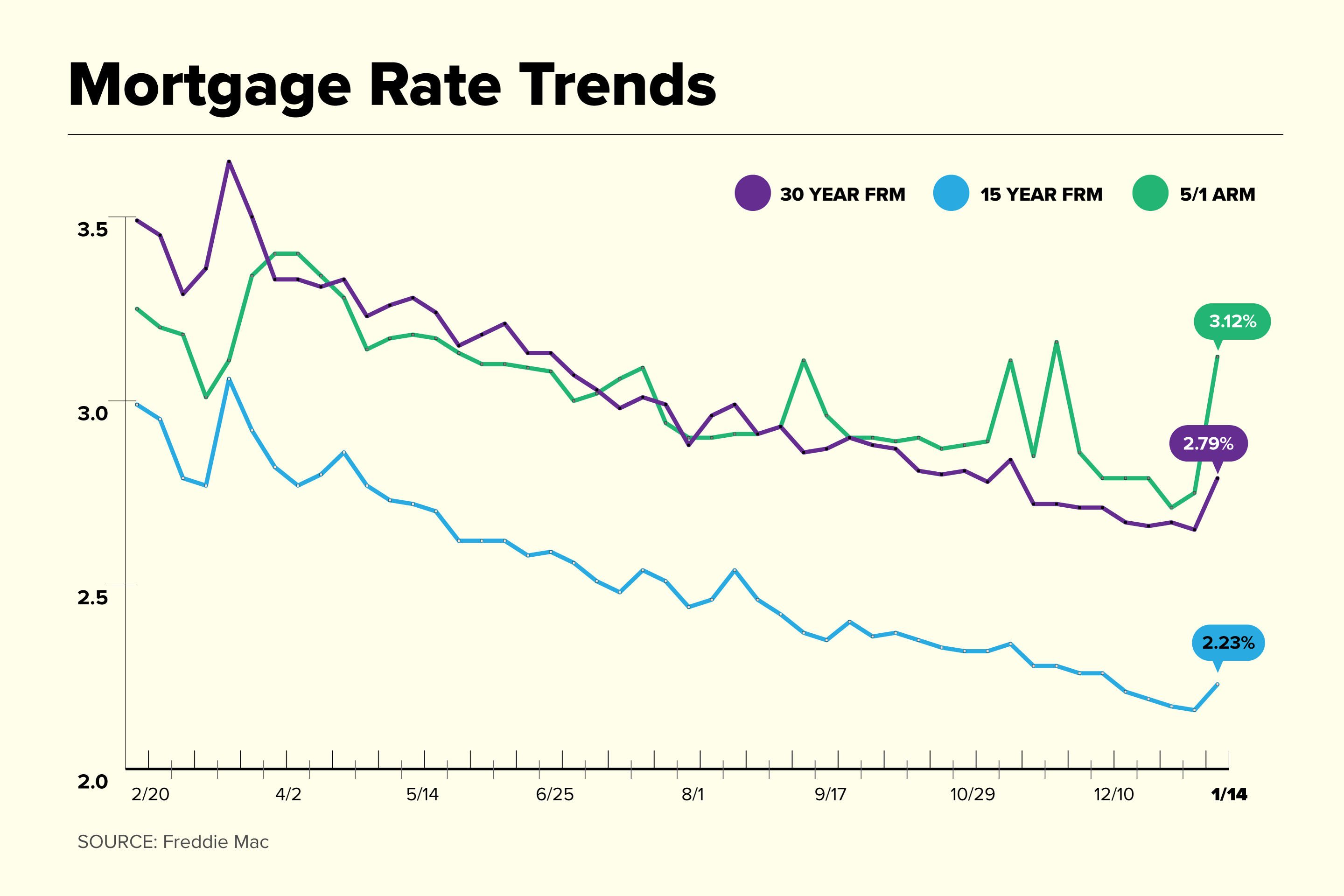

Current Mortgage Rates Trends

As of the latest data, mortgage rates have shown signs of stabilization after recent fluctuations. Experts predict modest increases in the coming months, driven by anticipated economic growth and inflationary pressures.

According to Freddie Mac, the average 30-year fixed-rate mortgage currently stands at [insert recent rate]. While rates remain relatively low by historical standards, they are gradually climbing as the economy recovers from pandemic-related challenges.

Historical Comparison

- 1980s: Mortgage rates exceeded 15% due to high inflation.

- 2010s: Rates dropped below 4%, fueled by Federal Reserve interventions.

- 2023: Rates hover around [insert current rate], reflecting a balanced market.

How to Compare Mortgage Rates

Comparing mortgage rates requires careful consideration of multiple factors beyond the interest rate itself. Loan terms, fees, and APR (annual percentage rate) all contribute to the total cost of borrowing.

Key Factors to Consider

- Interest Rate: The primary cost of borrowing.

- APR: Includes interest rate and additional fees, providing a more accurate cost comparison.

- Loan Terms: Fixed vs. adjustable rates, repayment periods, and prepayment penalties.

Using Online Tools

Many financial websites offer mortgage calculators and comparison tools to help borrowers evaluate different loan options. These resources allow you to input specific details and receive personalized rate estimates based on current market conditions.

Tips for Getting the Best Mortgage Rates

Securing the best mortgage rates involves strategic planning and proactive steps. Follow these tips to maximize your chances of obtaining favorable terms:

Improve Your Credit Score

Paying bills on time, reducing debt, and disputing errors on your credit report can boost your score, making you a more attractive borrower.

Shop Around

Don't settle for the first offer you receive. Compare rates from multiple lenders to ensure you're getting the best deal. Consider both traditional banks and online lenders for a comprehensive comparison.

Lock in Your Rate

If you find a favorable rate, consider locking it in to protect against potential increases during the loan approval process. Rate locks typically last 30-60 days, providing peace of mind during closing.

Common Mistakes to Avoid

Making uninformed decisions can lead to unfavorable mortgage terms and higher costs. Avoid these common pitfalls to optimize your borrowing experience:

Ignoring Additional Fees

Loan origination fees, closing costs, and private mortgage insurance (PMI) can add up quickly. Always review the full breakdown of costs before committing to a loan.

Not Shopping Around

Accepting the first rate offer without exploring alternatives can result in missed opportunities for better terms. Take the time to compare multiple lenders and negotiate for the best deal.

The Future of Mortgage Rates

Looking ahead, mortgage rates are expected to continue their gradual upward trend as the economy strengthens. Experts anticipate moderate increases over the next few years, driven by inflationary pressures and anticipated Federal Reserve actions.

Homebuyers should consider locking in current rates if they align with their long-term financial goals. While rates may rise, they remain relatively low compared to historical averages, making now an opportune time to secure financing.

Conclusion and Next Steps

Understanding current mortgage rates empowers you to make informed decisions about one of the most significant investments of your life. By staying informed about market trends, comparing loan options, and taking proactive steps to improve your financial standing, you can secure the best possible mortgage terms.

Take action today by reviewing your credit report, exploring loan options, and consulting with trusted lenders. Share your thoughts or questions in the comments below, and don't forget to explore our other articles for more valuable insights into homeownership and finance.

Disclaimer: The information provided in this article is for educational purposes only and should not be considered financial advice. Always consult with a qualified professional before making financial decisions.

- Best Restaurants Near Nederlander Theater Nyc

- Ed Edd And Eddy The Kanker Sisters

- Chucky Series Characters

- Christmas Tree With Glass Icicles

- Puro Pfp

Current Mortgage Interest Rates

Current Mortgage Rates Rates Jump Higher Money

Current Mortgage Rates Today 2025 Piers Mcgrath